Insurers on the London Stock Exchange using only the IFRS 17 Premium Allocation Approach are valued in quite a different way to those who aren't, and there is a lot of value and insights to be gained from grouping them together, and looking at them seperately from their GMM/VFA cousins. But there are only a few 100% PAA'ers on the LSE!

Net insurance service result (ISR) as a percentage of insurance revenue to 30 June 2023.

Reinsurance net expenses on business ceded equals recoveries less reinsurance premiums. Don't panic about Lancashire's high reinsurance expense %, they have an even higher ISR margin.

Forward earnings yield based on double the interim earnings over the 6 months to 30 June 2023; with the negative earnings yield for Direct Line Insurance indicating tough pricing conditions in UK motor.

Don't think I've ever shared stock tips here , so, I'm not going to start, but if I had a bit of spare cash; I'd have a close look at #ConduitHoldings (LON:CRE), a Bermuda-based pure play #reinsurer, listed on the London Stock Exchange, as they tick a number of boxes:

1. Execs are buying!

2. Price to book just over parity (value investors take note!)

3. Decent risk adjustment at 80%

4. Discounting their LIC at the lowest (most conservative) rates of the LSE PAA insurers.

5. Forward earnings yield of 17%

I'd prefer them not to be deferring acquisition costs, but this is easily adjusted for, and the price to book is still decent.

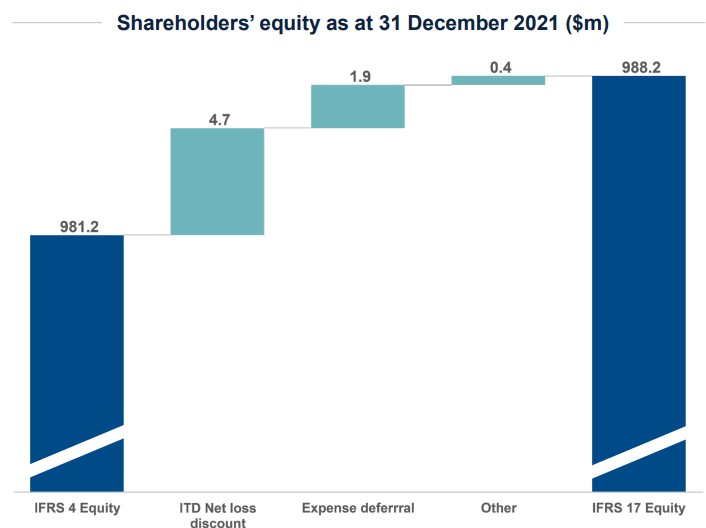

The following factors resulted in an increase to shareholders' equity:

The net impact of discounting the LIC was an increase of $4.7m.

Further deferral of acquisition related operating expenses resulted in an increase of $1.9m.

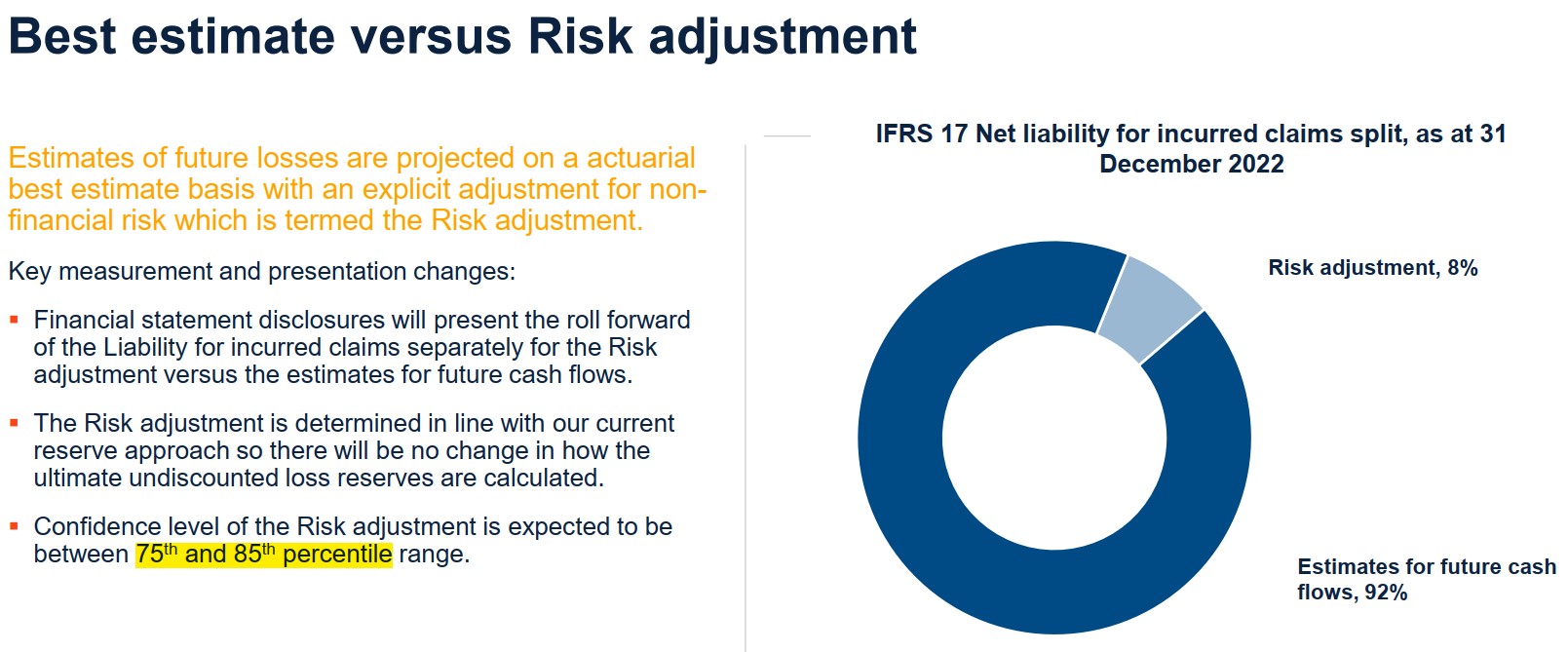

"No change to the approach to setting the Risk adjustment"

Other measurement changes include a "revaluation of items previously recorded as non-monetary under IFRS 4 and provision for non-performance risk on ceded reinsurance recoveries".

Conduit Holdings indicated a much larger ($53m) difference between IFRS 4 and IFRS 17 shareholders' equity on 31 Dec 2022 (than 31 Dec 2021, only $7m), largely as a result of movements in interest rates during 2022.

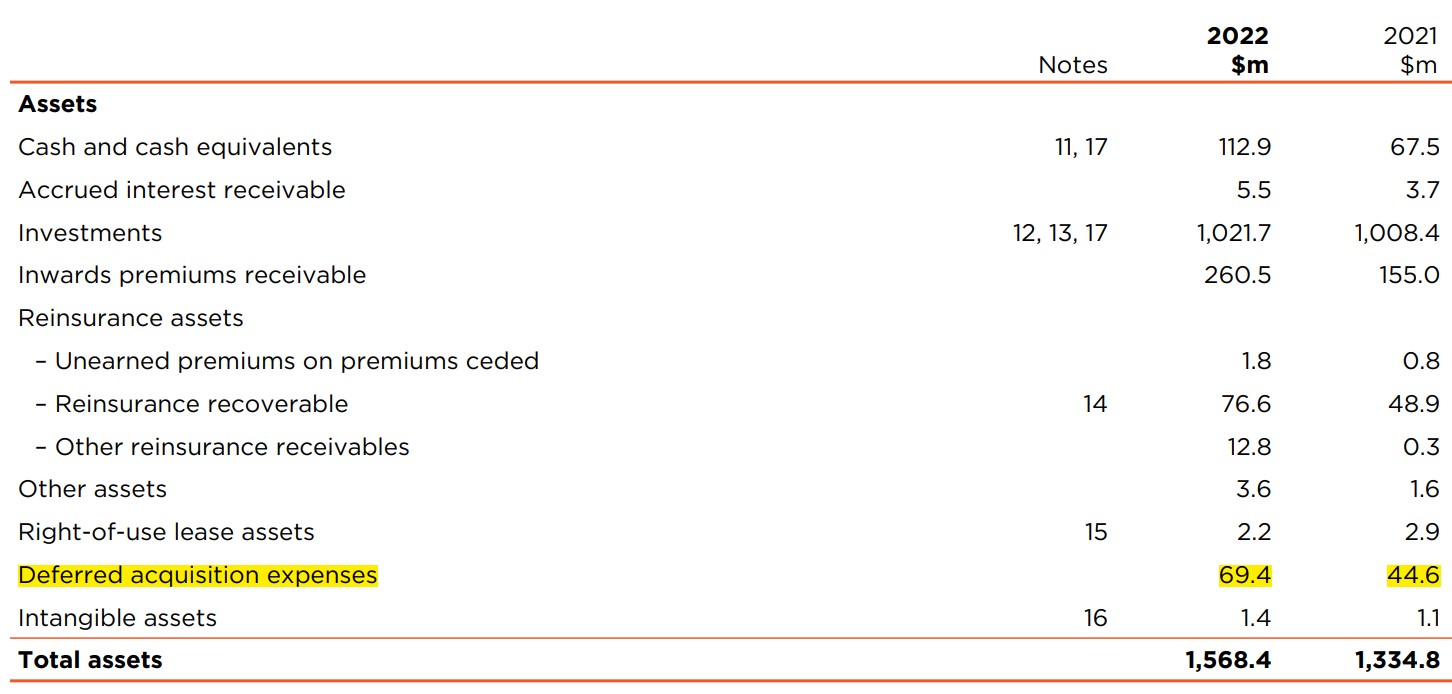

With Conduit's acquisition costs being deferred, it's important to get a handle on them. A start are their IFRS 4 deferred acquisition cost assets:

Hot off the press are the first real and fresh (but unaudited!) IFRS 17 interim results to 30 Jun 2023. Caveat: IFRS17 allows insurers to take different accounting options, which mean shareholders' equity is not calculated on a comparable basis from insurer to insurer. So a-levelling playing fields we will go!

Based on the above a very adjusted IFRS17 equity can be calculated:

Of course the risk adjustment is there to compensate for taking on non-economic risk, so booking it to profit would only make sense if you didn't feel that you need to be compensated for non-economic risk! So, treat these numbers as me kicking around ideas, it's certainly not my final thought on this, as investors demand compensation for risk, the question is how much is appropriate (maybe vary across different lines of business) and how do we adjust for it from what is disclosed.

NB to note that there are other adjustments which need to be made (beyond the above) to allow for a fair comparison. We'll delve into that in due course, but this is enough for today.

IFRS 17 allows insurers some latitude in determining discount rates, and there's particular subjectivity in deciding on what illiquiditypremium to inlude. In the image below we can see the GBP discount rates being used by Conduit Holdings, Lancashire Holdings and Sabre Insurance; for 1, 3 and 5 year periods. The longer the period the bigger a difference in discount rates make, over 5 years the discount factors with which cashflows would be multiplied are:

Note that this only compares the GBP rates, some insurers also use rates in other currencies, and for Lancashire Holdings I suspect the USD rates are more important than the GBP discount rates.

There are many accounting choices and assumptions which would result in 2 insurers, who are identical in ever way, having different shareholders' equity; e.g.

If events unravel as expected, the amount accounted for as risk adjustments will flow through to profit. It is therefore key to get a handle on how much each insurer is accounting for as a risk adjustment. Some insurers will exercise accounting choices to allow lower risk adjustments and more to flow through to equity now, whilst other insurers are more prudent.

For these PAA insurers it's likely that most, if not all, of the risk adjustments are part of their liability for incurred claims (LIC).

Conduit Holdings disclosed that their risk adjustment formed 8% of their total LIC on 31 Dec 2022; which corresponds to a risk adjustment which is roughly at the 80th percentile (the midpoint of their target range).

IFRS17 requires insurers to disclose the percentile at which their risk adjustments lie. Here's the disclosure info of the LSE's PAAs (at the time of writing, 11 Aug 2023, note that for some insurers we're still awaiting their disclosure):

Admiral Group has chosen the highest risk adjustment percentile of the PAA insurers on the London Stock Exchange, 93%, and Direct Line the lowest of those currently disclosed, at 75%; with Lancashire Holdings and Sabre Insurance still to disclose their exact percentiles. I could only find Hiscox's percentile for 31 Dec 2022 (not 31 Dec 2021) of 78%. It's possible that I the percentiles are lying around somewhere, and I haven't dug around hard enough.

To compare insurers' shareholders' equity on a like-for-like basis, we need to either:

We can see that for London Stock Exchange insurers following solely the Premium Allocation Approach, there were no huge movements in shareholders' equity at 31 Dec 2021, as the premium allocation approach is similar to the valuation methodology they were previously using.

The main issues impacting Admiral's shareholders' equity were:

Events Not in Data (ENIDs), the details of this are not clear.

Discounting of claims.

Not clear whether discounting to time of incurrence or to discounting the LFRC as well.

Solvency II risk free rate + illiquidity premium (bottom-up)

Changes in discount rate disaggregated between P&L and OCI to match movement in the fair value of assets

Risk adjusment: around 90th percentile

Acquisition costs expensed, no deferral

Onerous contracts

With Hiscox's acquisition costs being deferred, it's important to get a handle on them. A start are their IFRS 4 deferred acquisition cost assets:

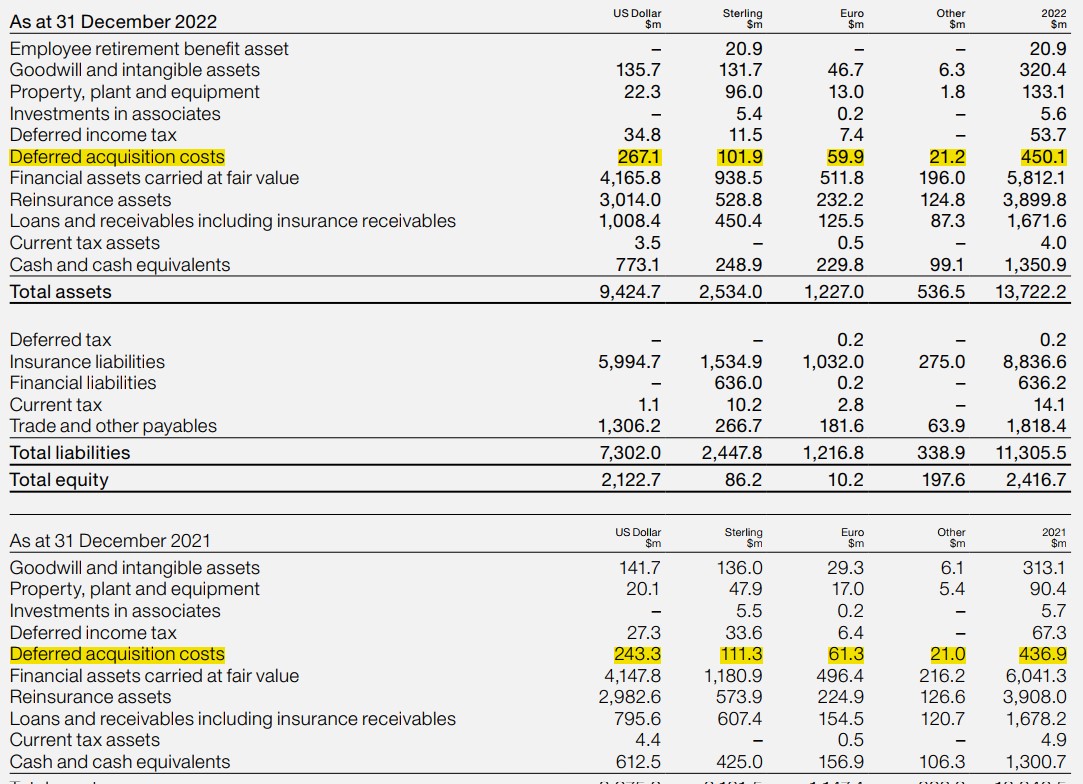

With Lancashire's acquisition costs being deferred, it's important to get a handle on them. A start are their IFRS 4 deferred acquisition cost assets:

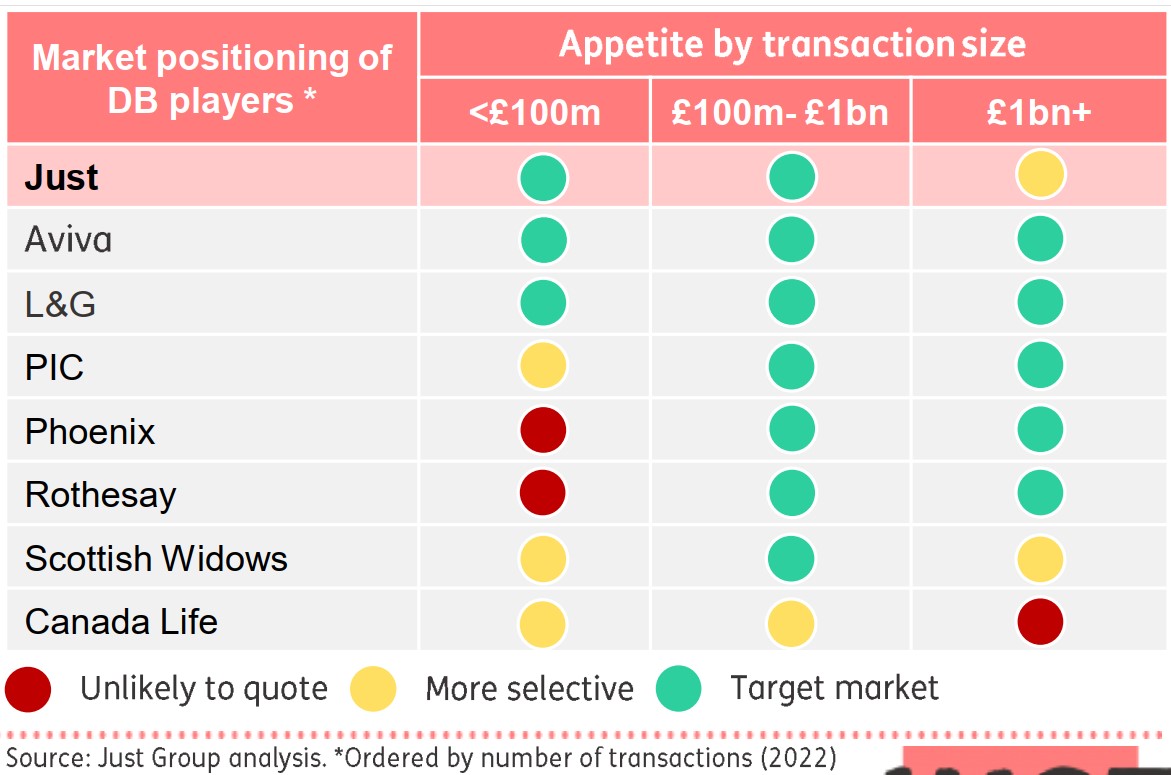

Interesting list of players in the DB derisking transaction market, compiled by Just Group:

For legal reasons please consider everything written on this website to be for entertainment purposes alone. It's vitally important to question everything and apply your own mind.